Smart Option Credit Card

Our lowest available interest rate and no annual fee

Do more with lower interest

Our smart option credit card puts you in charge. Consolidate your credit with low interest, no annual fee and added protection wherever you make purchases.

Forget the fees

Pay no annual fee and get our lowest interest rate.

Enjoy benefits

Convenient credit card benefits help protect you and your purchases.

Balance transfer

Use our introductory offer on balance transfers to consolidate your debt.

Big purchases, smart options

Manage your spending or consolidate higher interest rate balances on our lowest-rate, no fee credit card.

Is a credit card balance transfer worth it? See how much you can save.

Card details and transaction fees

Balance transfers

0% introductory APRD for the first 12 monthsD on balance transfers, then variable purchase rate of 14.24% to 23.24% based on creditworthiness applies

Purchase rate

Variable 14.24% to 23.24% APR based on creditworthiness

Cash advances

Variable 26.24% to 29.24% APR based on creditworthiness; each transaction is subject to a 5% fee (minimum $10)

Annual fee

$0 with this no-fee credit card

Pay with your phone

Add your cards to your mobile device and pay securely with Digital Wallet.

Get alerts

Track your accounts and transactions with text and email alerts.

Pay your bills

Automate your bill payments with Digital Banking for extra peace of mind.

Not quite sure? Answer a few questions to find the right credit card for you.

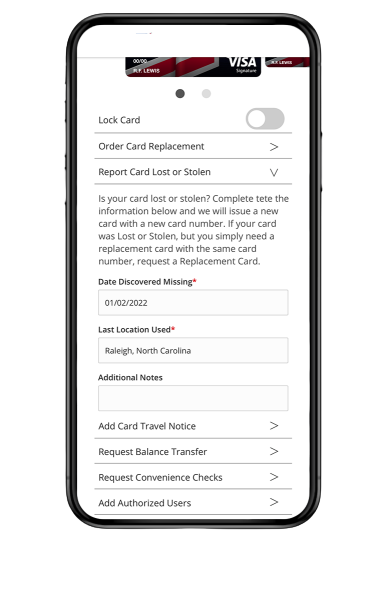

Access any of our card services from your phone

Temporarily lock your card

Report a lost or stolen card

Notify us if you're traveling

Access any of our card services from your phone

Temporarily lock your card

Access any of our card services from your phone

Report a lost or stolen card

Access any of our card services from your phone

Notify us if you're traveling